Dividend by EPF Malaysia for year’s

March 7, 2023 / 0 comments / 1139 views / Tags: dividend, Employee Provident Fund, KWSP, Malaysia / Category: Article and lifestyle

Dividend by EPF Malaysia

Dividend announced by EPF Malaysia a dividend rate of conventional saving and 4.75% for Syariah account.

The table chat

| Year | Conventional | Syariah |

| 2023 | 5.5% | 5.4% |

| 2022 | 5.35% | 4.75% |

| 2021 | 6.1% | 5.65% |

| 2020 | 5.2% | 4.9% |

Semakan Dividen

EPF member are able to check the amount of dividends 2022 that have been credit into statement account from March 4, 2023 online .

Guarantee Dividend

The guarantees a minimum of 2.5% for Conventional account through approve investments to ensure that your saving are secured.

Annual payout is credit based on your savings as at 1st January yearly and calculate based on your daily aggregate balance.

Mandatory and voluntary

Under voluntary Individual employed, self-employ or business owners are eligible to contribute based on their own requirement.

Whereas your monthly contribution will earn dividend base on day’s in the month of said contribution until the end of that year.

Mandatory Rate

11% Employee compulsory contribute rate.

13% Employers Compulsory contribute rate ( salary RM5,000 & below)

12% Employers compulsory contribute rate ( salary RM5,000 & above)

Annual Tax Exemption

Tax-deductible up to a maximum amount of RM4,000 or more subject to amendments ( if any) by the government.

Withdraw of EPF Savings are free from paying income tax and returns on the EPF investment are also tax-exempted.

马来西亚公积金局的股息 马来西亚公积金局的股息宣布其 2022 年传统储蓄的股息率为 5.35%,伊斯兰教的股息率为 4.75%, 公积金局会员可以在线查看从2023年3月4日起存入报表账户的2022年股息金额. 公积金局通过批准的投资为常规账户提供至少 2.5% 的保证,以确保您的储蓄有保障, 年度支出是根据您每年 1 月 1 日的储蓄计算的,并根据您的每日总余额计算. 在自愿的情况下,受雇个人、个体经营者或企业主有资格根据自己的要求缴款, 而您的每月供款将在该供款月份的当天赚取股息,直至该年年底. 根据政府的修订(如果有),最高可扣税 RM4,000 或更多, 提取公积金储蓄无需缴纳所得税,公积金投资的回报也免税.

Property Investment in Malaysia year’s 2023

February 12, 2023 / 0 comments / 875 views / Tags: Apartment for rent, Apartment for sale, Bukit Jalil, condominium for sale, IOI resort city / Category: Article and lifestyle

Property Investment in Malaysia

- Malaysia economic is expected to continued growth in year’s 2023 which can lead to increase the demand of properties and potentially drive up the property prices.

- Medium-low interest rates are easier, advantage and more affordable for individuals to obtain financing for property purchases.

- Malaysia government has implement various incentives to encourage investment to the property market included tac incentives and foreign ownership restrictions.

- Government Significant allocate in infrastructure including transportation and communications can improve the livability and property demand of the country.

- By increasing number of tourists visiting Malaysia after MCO, there is potential for rental income from properties in tourist hotspots.

- Also by increasing number of businesses there is demand of industrial property .

- Wide range of property options providing opportunities for investment in various segment including industrial, residential, commercial and land .

Several advantages Investing in property

- The value of property will appreciate over time, it’s providing potential source of long-term wealth.

- Properties could generate rental income providing a steady source of passive income.

- Diversify your investment portfolio reducing your overall rick.

- Unlike stocks or share, Property is a tangible asset that physically see and touch.

- As the cost of living are increases over time, the rental income could help keep pace in inflation.

- You have more control over your investment as an owner to Sell and Rentals.

Investment hotspot

Purchasing property in Bukit Jalil and IOI Resort City could offer several benefits

- Bukit Jalil is w well established residential area located in the heart of Kuala Lumpur while IOI Resort City is a well-planned, integrated resort city located in the south part of Selangor. Both areas offer convenient access to various amenities like shopping malls, international school, golf club and medical facilities.

- With the demand for property in these areas increase, the value of property likely to increase over time that providing potential for your capital appreciation.

- Properties in Bukit Jalil and IOI Resort City are high in demand making them a good investment option to generate capital increment and rentals income.

- IOI Resort City offers a range of lifestyle amenities including Parks, golf courses, shopping mall and retails which could provide a high quality of life for residents.

- Bukit Jalil and IOI Resort City are undergoing significant development, with plan for further improvements and expansion in the future.

In Summary

Education Hub

Malaysia is home to a variety of higher education institutions, including public and private universities, international branch campuses, and colleges. These institutions offer a wide range of programs, making Malaysia an attractive destination for both local and international students.

Beautiful Country

Malaysia’s tropical climate provides year-round warmth and greenery, making it an ideal destination for those seeking a pleasant and lush environment.

Medical hub

Malaysia was emerging as a popular destination for medical tourism since 2021 and was on its way to becoming a medical hub in the region

My Second Home Program

Initiative launched by the Malaysian government to attract foreign retirees, expatriates, and long-term visitors to make Malaysia their second home.

Delicious foods

Malaysia is renowned for its delicious and diverse food offerings. The country’s culinary scene is a reflection of its multicultural population, blending flavors from Malay, Chinese, Indian, and indigenous cuisines that cater to a wide range of tastes and preferences

Selangor state government Welfare Malaysia

November 8, 2022 / 0 comments / 1896 views / Tags: Article, Lifestyle, Malaysia, Selangor citizen welfare / Category: Article and lifestyle

Selangor state government welfare

Did you know the benefits giving by The Selangor State Government Malaysia SSIPR to ALL it’s citizens. ( T&C apply) .

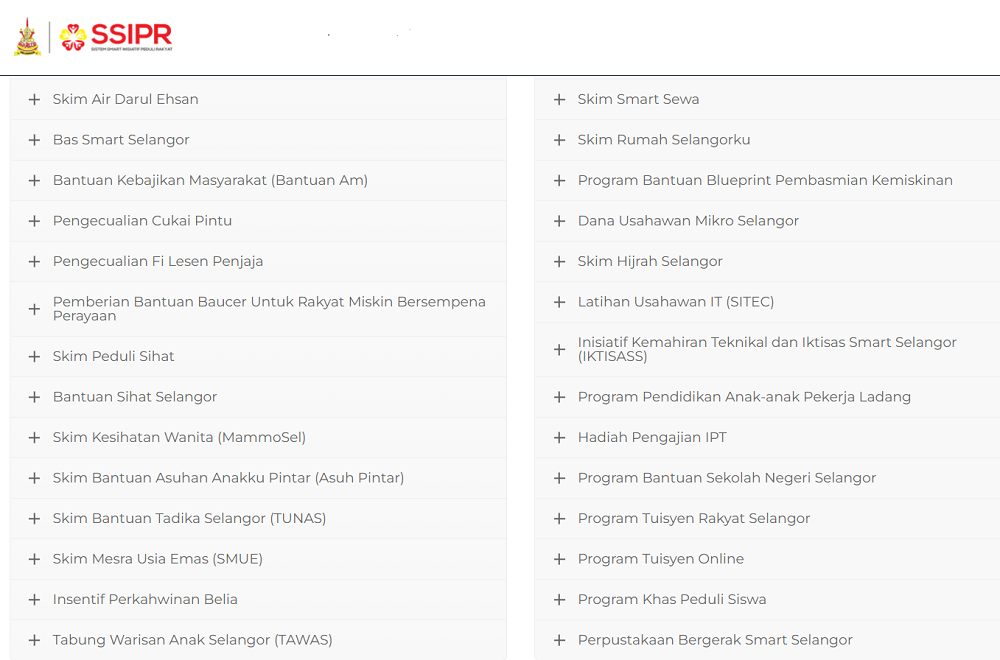

SSIPR Selangor

- New born baby Rm1,500

- Golden Age friendly scheme Rm100 monthly

- Preschool Rm50 monthly

- Free tuition classes

- Rm1,000 when you enter College / University

- Funeral expenses Rm2,500

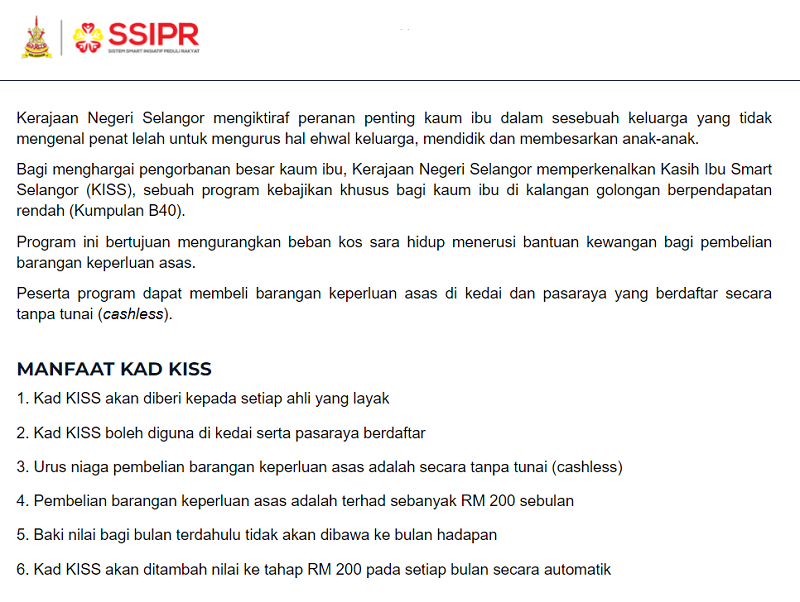

- KISS RM200 monthly Basic Necessity for B40 mothers group

- Bus Smart Selangor

- Benefit Program up to RM350

- Free Mammogram checkup

- Up to Rm500 yearly Medical expenses

- 0% interest Business loan up to Rm30,000

- Free internet access – WIFI Smart

雪兰莪州政府给予所有公民的福利.(条款和条件适用) 新生婴儿 Rm1,500 黄金时代友善计划每月 Rm100 学前班每月 RM50 免费补习班 当你进入学院/大学时 RM1,000 丧葬费 Rm2,500 KISS 每月 RM200 , B40 妈妈组基本必需品 免费巴士 高达 RM350 的福利计划 免费乳房 X 光检查 每年高达RM500的医疗费用 0% 利息商业贷款高达 Rm30,000 免费上网 - WIFI 智能

KISS – kasih Ibu Smart Selangor

To appreciate the great sacrifice of mothers, the Selangor State Government introduced a special welfare program among low-income groups B40.

为了感谢母亲们的巨大牺牲,雪兰莪州政府推出了一项针对低收入群体 B40 的特殊福利计划.

Bus Smart Selangor

The Selangor State Government has provided free bus services to to 3 Selangor Authorities namely Shah Alam City Council (MBSA) , Subang Jaya Municipal Council (MPSJ) and Klang Municipal Council (MPK).

雪兰莪州政府已向 3 个雪兰莪州政府提供免费巴士服务,即莎阿南市议会 (MBSA)、梳邦再也市议会 (MPSJ) 和巴生市议会 (MPK).

Benefit Program

Provision of temporary assistance given to eligible Selangor citizens up to RM350 per month to obtain basic needs in case of unavoidable life problem.

每月向符合条件的雪兰莪州公民提供高达 350 令吉的临时援助,以满足在不可避免的生活问题时的基本需求.

Voucher assistance

You can obtain vouchers specifically for low-income people in the State of Selangor to buy essential items for Hari Raya Aidilfitri , Chinese New Year and Deepavali celebrations.

您可以获得专门针对雪兰莪州低收入人群的优惠券,以购买开斋节、农历新年和屠妖节庆祝活动的必需品.

Health Care Insurance Scheme

Under the Health Care Insurance Scheme program, policy holders are entitle to basic health treatment benefits every year and basic coverage covering death, accident and critical illness coverage.

根据医疗保险计划计划,保单持有人每年都有权获得基本医疗福利和包括死亡、意外和重大疾病保险在内的基本保险.

Mammogram Scheme

Under the Women’s Health Scheme providing free mammogram screening services to all women in the State of Selangor.

根据妇女健康计划,为雪兰莪州的所有妇女提供免费的乳房 X 光检查服务.

Healthy Help ( Bantuan Sihat )

This program to help low income Selangor citizens to get healthy treatment for minor surgery , Kidney dialysis , eye cataracts , prosthetic legs and other treatments that will be considered.

该计划旨在帮助雪兰莪低收入公民获得小手术、肾透析、眼白内障、假腿和其他可以考虑的治疗的健康治疗.

Rumah Selangorku Scheme

Eligible Selangor Citizens can apply to own house worth no more than RM250,000 through the Rumah Selangorku Scheme.

符合条件的雪兰莪公民可以通过 Rumah Selangorku 计划申请拥有价值不超过 RM250,000 的自己的房屋.

Technical & economic initiative

Smart Selangor Technical Skills and economic Initiative Program is a technical certification course where fees are fully covered by the Selangor State Government included fix allowance of RM300 per month.

Smart Selangor Technical Skills and Expertise Initiative Program 是一项技术认证计划,学费由雪兰莪州政府全额支付,另外还有每月 300 令吉的额外津贴.

Fund Scheme

Through this scheme the Selangor State Government will buy houses and Rent them out to low-income buyers. The house will be sell with the selling price minus a portion of the Rental paid. Participants of this program can carry out the purpose of purchasing the house unit in question within a period not exceeding 25 years at the original price of the house starting from the date it was first rented.

通过这项计划,雪兰莪州政府将购买房屋并将其出租给低收入买家。然后房子将以售价减去已付租金的一部分出售。该计划的参与者可以在不超过 25 年的期限内以房屋最初出租之日起的原价购买有关房屋单元的目的.

Smart Rent Scheme

The Smart Rent Scheme provides opportunities for low and medium-low income groups who are unable to make purchases,. Rumah Selangorku offered a Rental Scheme at a reasonable and affordable rate so that they can finally owned their own home in the State of Selangor.

智能租金计划为无法购买的中低收入群体提供了机会。 Rumah Selangorku 以合理且负担得起的付款率提供租赁计划,以便他们最终可以在雪兰莪州购买自己的房屋.

Applicable Benefits category

BKM – Malaysian Family Assistance

March 4, 2022 / 0 comments / 1508 views / Category: Article and lifestyleBKM – Bantuan Keluarga Malaysia

What is a BKM

BKM is a Government cash assistance to the needy to alleviate the cost of living and the burden of Low income citizens targeting groups for B40 households and singles, seniors and single parents.Payments will be make 4 times a year .

Categories

- Marriage applicants aged 59 years and BELOW with / without household income below RM2,500

- Marriage applicants aged 59 years ABOVE with income between RM2,501 – RM5,000

- Additional amount of RM300 for marriage Senior Citizens ABOVE aged 60 years old with / without household income in between RM0 – 5,000

- Additional amount of IBT RM500 for SINGLE PARENT who’s has children with / without household income RM0 – RM5,000

- Single unmarried and Single Parents ( IBT ) aged 59 years and below with No Children – Household income RM0 – RM5,000

Who’s eligible

- Single Parents with eligible children, house income RM5,000 and below

- Single Senior Citizen aged 60 years above who’s did not have children with household income less then RM5,000

- Single Citizen aged between 29 – 59 years with household income less then RM2,500

How to apply BKM

If you are an BPR 2021 recipient, BKC B40 recipient and BPR 2021 applicant who’s did not pass on the groups of receiving GKP you will be automatically taken into the BKM system for eligibility verification. If you have never applied for an ACA or BKC ( you should have no record in the IRBM’s database) you could make a new application through BKM brand / portal , satellite office, revenue service center and Urban transformation Center (UTC) .

Next :

BKM - 马来西亚家庭援助 BKM 是政府为有需要的人提供现金援助,以减轻生活成本和低收入公民的负担,目标群体为 B40 家庭和单身、老年人和单亲父母。每年支付 4 次. 类别 1)59岁及以下的婚姻申请人,家庭收入低于RM2,500 2)年龄在 59 岁以上且收入介于 RM2,501 至 RM5,000 之间的婚姻申请人 3)60 岁以上的长者结婚加额 RM300,家庭收入在 RM0 - 5,000 之间 4)有/没有家庭收入 RM0 - RM5,000 的孩子的单亲父母的额外 IBT RM500 5)59 岁及以下没有孩子的单身未婚和单亲父母 (IBT) - 家庭收入 RM0 - RM5,000 谁可以申请 *有符合条件的孩子的单亲父母,房屋收入 RM5,000 或以下 *60岁以上的单身长者,没有孩子,家庭收入低于RM5,000 *29-59岁的单身公民,家庭收入低于RM2,500 如果您是 BPR 2021 接收者、BKC B40 接收者和 BPR 2021 申请人,但未通过 GKP 接收组,您将自动进入 BKM 系统进行资格验证。如果您从未申请过 ACA 或 BKC(您应该在 IRBM 的数据库中没有记录),您可以通过 BKM 品牌/门户、卫星办公室、收入服务中心和城市转型中心 (UTC) 进行新的申请。

Home Ownership Campaign 2020

June 17, 2021 / 0 comments / 1428 views / Tags: Article, Lifestyle / Category: Article and lifestyleHome Ownership Campaign

Home Ownership Campaign HOC was a government initiative designed to support home buyers looking to purchase property. At the same time, it also encouraged the sales of unsold properties in Malaysia’s housing market .

With growing desire for home ownership among-st Malaysians, particularly in popular urban areas, the HOC initiative was designed to match aspiring home-seekers with all those empty homes.

The Home Ownership Campaign (HOC), which ran throughout 2019, was designed to encourage the increase in home ownership among Malaysians. And now, it’s back again from June 2020 till 2021.

The financial incentives & benefit that were offered as part of the scheme.

Full stamp duty exemption till RM1 million

Under the scheme, successful applicants enjoyed 100% stamp duty exemption on Instrument of Transfer for any residential home purchase up to the value of RM1 million.

Partial stamp duty exemption till RM2.5 million

For properties worth more than RM1 million up to RM2.5 million, you paid 3% stamp duty on the Instrument of Transfer for the amount that’s more than RM1 million.

| Property Prices | Stamp Duty |

| First RM100,000 | Exempted |

| RM100,001 to RM500,000 | Exempted |

| RM500,001 to RM1,000,000 | Exempted |

| RM1,000,001 to Rm2,500,000 | 3% |

How do you save on it ?

assume your property purchased price was RM500,000 in between with & without HOC scheme.

| without HOC | with HOC | |

| Down payment (500,000 x 10%) | RM50,000 | RM0 |

| Stamp duty on loan (450,000 x 0.5%) | RM2,250 | RM0 |

| Stamp duty on MOT (100,000 x 1% + 350,000 x 2 %) | RM8,000 | RM0 |

| Total cost | Rm60,250 | RM0 |

Comparison chat

Stamp duty exemption on the instruments of transfer and loan agreement for the purchase of residential homes priced between RM300,000 to RM2.5 million (subject to at least 10% discount provided by the developer).

The exemption on the instrument of transfer is limited to the first RM1 million of the property price, while full stamp duty exemption is given on loan agreement effective for Sale and Purchase Agreement (SPA) signed between 1st June 2020 to 31st May 2021.

Instruments on secure loan exemptions.

Instruments on secure loan exemptions.

All properties within the scheme enjoyed a further stamp duty exemption on the Instrument of Securing Loan up to Rm2,500,000 purchase price.

Eligibility (term & conditions)

The Home Ownership Campaign covered registered residential properties with a value between RM300,000 and RM2.5 million. Those properties must be registered with the relevant authority for each region. it’s important to note that properties classified as a SoHo, SoFo, or SoVo were not qualified for the HOC either.

Eligibility only applies to those registered residential properties listed by developers within the scheme. covered registered residential properties with a value between RM300,000 and RM2.5 million. Those properties must be registered with the relevant authority for each region.

Know more about home ownership campaign 2020

Know more about home ownership campaign 2020

Does it apply to secondary markets?

No, the HOC 2020 only applied to new properties registered under the campaign from specific developers.

Did all properties receive a 10% discount?

A minimum 10% discount applied on all properties within the scheme, with the exception of those subject to government price controls.

Can I buy multiple properties under the campaign?

Yes, you can. There was no limit to the number of properties you can purchase, and get stamp duty exemptions for all, under the HOC 2020.

Do I have to pay a fee to participate?

No, the campaign is free. Developers must pay a registration fee but that does not apply to home owners.

What was the exemption amount on the Instrument of Loan?

The exemption on an Instrument of Loan amount covers 0.5% of the loan agreement. That amount covers the standard stamping fee for such an instrument.

**Details of the home ownership campaign 2020 will be updated upon the official release of government gazette.

政府将会再度推出“拥有房屋运动”计划,购买房屋价格介于30万至250万令吉之间将可豁免地契 转让及贷款合约的印花税。至于地契转让方面,免印花税仅限于房屋价值的首100万令吉。

这项豁免 适用于今年6月1日至2021年5月31日之间签订的买卖协议,但须遵守发展商给予至少10%折扣的条款。

Employee Provident Fund Malaysia – death Benefit and withdrawal

March 29, 2021 / 0 comments / 2632 views / Tags: death withdrawal, Employee Provident Fund, EPF, Malaysia / Category: Article and lifestyle

Employee Provident Fund

Death Benefit

Employee Provident Fund – Death Benefit is a gesture of compassion by the EPF to it’s member’s next-of-kin (under EPF’s discretion). A one-time payment of RM2,500 will be considered and awarded to any of the deceased member’s eligible dependents.

All member are being encourage to do a nomination to your beneficial earlier to enable your next-of-kin to withdraw your EPF saving without COMPLICATIONS.

Member’s dependent will also be considered for the death benefit to support they go through the difficult time.

Death Withdrawal Conditions

- Deceased member is Malaysian including Permanent Resident and Non- Malaysian

- Member’s dependent of Parents / window / children / widower

- Received application within 6 months from the date of pass away

- For member who’s pass away aged 60 years below

- Provided still have saving balance into EPF account

Document needed to apply

- Form KWSP 9KM

- Bank account details ( Saving / Current / Bank’s verification letter / Estate account of the deceased )

- Declaration of Marriage Letter ( Non-Muslim member who’s married before 1 Marth 1982)

- Power of attorney ( Official letter issued by the Courts / Legal Institutions / Amanah Raya Berhad )

- Original and copy of identification documents

- Original and copy of Applicant’s Birth Certificate ( when required)

- Member’s Death Certificate or nominee’s Death Certificate if nominee has passed away.

- Member’s Birth Certificate OR Marriage Certificate OR divorce certificate if divorced.

- Recipient’s declaration of responsibility for Muslim – Appendix A

- Recipient’s declaration of responsibility for Non- Muslim – Appendix B

Nominee

- Nominee 18 year old and above could apply for withdrawal

- If the nominee passes away, their next-of-kin are eligible to apply for Death Withdrawal for Muslim.

- If the nominee passes away before the death of member, the member’s next-of-kin is eligible to apply for death withdrawal but if the nominee passes away after the death of the member, the nominee’s next-of-kin are able to apply for Non-Muslim.

Without nominee

- For member who is Married – their widow / widower, children or their guardian, parents, siblings or administrator.

- For member who is UNMARRIED – their parents, siblings or administrator.

关于公积金会员身故赔偿 死亡抚恤金是公积金 EPF 对其成员的近亲(由公积金酌情决定)表示同情的一种姿态。将考虑一次性支付 RM2,500 并奖励给已故会员的任何合格家属. 我们鼓励所有会员尽早指定您的受益人,以使您的近亲能够在没有并发症的情况下提取您的 EPF 储蓄 ,会员的受抚养人也将被考虑获得身故抚恤金,以支持他们度过困难时期. 提款条件 1) 已故成员是马来西亚人,包括永久居民和非马来西亚人 2) 会员的父母/窗口/子女/窗口的家属 ,自会员去世之日起6个月内收到申请人申请 3) 60岁以下的过世会员 4) 仍然有储蓄在 EPF 帐户 申请所需文件 1) 表格 KWSP 9KM 和清单 2) 银行账户详细信息(储蓄/往来/银行的验证函/死者的遗产账户) 3) 结婚声明书(1982 年 3 月 1 日前结婚的非穆斯林成员) 4) 授权书(由法院/法律机构/Amanah Raya Berhad 发出的正式信函) 5) 身份证明文件正本及副本以供核对 6) 申请人出生证明的原件和复印件以供验证(如需要) 7) 会员的死亡证明或被提名人的死亡证明(如果被提名人已经去世)。 8) 会员的出生证明(如果未婚)或结婚证或离婚证(如果离婚)。 9) 收件人对穆斯林的责任声明 - 附录 A 10)收件人对非穆斯林的责任声明 - 附录 B 公积金提名人提款 1) 18岁及以上的被提名人可以申请提款 2) 如果被提名人去世,他们的近亲有资格为穆斯林申请死亡提款。 3) 如果被提名人在会员去世前去世,则会员的近亲有资格申请死亡提款,但如果被提名人在会员去世后去世,则被提名人的近亲有资格申请死亡提款非穆斯林。 公积金没有被提名人提款 1) 对于已婚会员 - 会员的遗孀/鳏夫、子女或其监护人、父母、兄弟姐妹或管理人。 2) 对于未婚成员 - 成员的父母、兄弟姐妹或管理员

Should You Buy A House in Year 2022

July 24, 2020 / 0 comments / 861 views / Tags: Article, market Info / Category: Article and lifestyleTo Buy a Home 2022

The start of a new decade often spurs people on to make financial decisions and goals, and if one of yours is to buy a house, you may be wondering whether 2022 is the right time to do so. The answer? It may depends.

Should i buy an investment property 2022 ?

Whether now’s the right time to buy a home should largely boil down to mortgage rates, low inflation, housing market inventory and your personal financial circumstances, Mortgage rates are recorded at an all-time low, 3.301% BR on a 30-year fixed mortgage.

Keeping the above in mind, this year could be the right one to buy a home .

Advantage when you

- You have good credit. Though it’s possible to qualify for a mortgage with a lower credit score, the higher yours is, the more likely you are to get approved for the most competitive rates available. And that could be your ticket to making home ownership more affordable.

- Your current debt load is manageable. Your debt-to-income ratio measures your monthly debt obligations relative to the income you bring in. The lower it is, the greater your chances of getting approved for a mortgage.

- But home loan approval aside, having less debt means you’re better equipped to take on the expense of a home, so rather than focus on that ratio alone, think about how you’re managing the debts you already have. If you can pay them easily, then taking on more debt in mortgage form is something you can likely swing, but if you’re already struggling, you may want to hold off.

- You have a solid amount of savings. You need savings to not only make a down payment on your home but also to keep up with its ongoing costs and buy yourself protection in the event of unplanned repairs. Ideally. On top of that, you should have enough money left over to cover three to six months of essential living expenses, housing costs included.

- You have a steady job. If you’ve been with the same company for years, have a good reputation, and have reason to believe your job is stable, then this year may be a good one to buy. But if you’re not confident in your job situation, it definitely pays to wait a few years, get settled at a new company or in a new career, and then move forward with your home buying plans.

REAL PROPERTY GAIN TAX MALAYSIA

June 8, 2020 / 0 comments / 18592 views / Tags: Article, market Info / Category: Article and lifestyle

Gains tax act 1976 the Real Property Gain Tax (RPGT) is a tax chargeable on the profit gained from the disposal of a property’s in Malaysia which is payable by a seller.

Malaysia Real Property Gain Tax

For example, A man bought a piece of property in year 2000 at a value of RM500,000. Subsequently, A man sold the property to A girl at the value of RM700,000 then the RPGT is calculated for RM200,000 profit gaining from the disposal of the property.

Deductible of gain tax after

- Renovation costs

- Stamp duty

- Valuation fees

- Legal fees, Agent fees

Malaysian & PR (Individual)

- Disposal within 3 years from purchased 30%

- Disposal 3 to 4 years from purchased 20%

- Disposal 4 to 5 years from purchased 15%

- Disposal after 5 years from purchased Nil

Malaysian & PR (Company)

- Disposal within 3 years from purchased 30%

- Disposal 3 to 4 years from purchased 20%

- Disposal 4 to 5 years from purchased 15%

- Disposal after 5 years from purchased 5%

Tax Rate of RPGT for foreigners (individual)

- Disposal within 5 years from purchased 30%

- Disposal after 5 years from purchased 5%

Exemptions

- An individual will be given an exemption equal to Rm 10,000 or 10% of the chargeable gain, whichever is greater.

- Malaysian citizen and permanent resident will be entitle once in a lifetime exemption on any chargeable gain arising from the disposal of his private residence

- Transfer and transmission from deceased to beneficiaries

- Transfer between Spouses, parent and child, grandparent and grandchild

- Transfer to trustees.